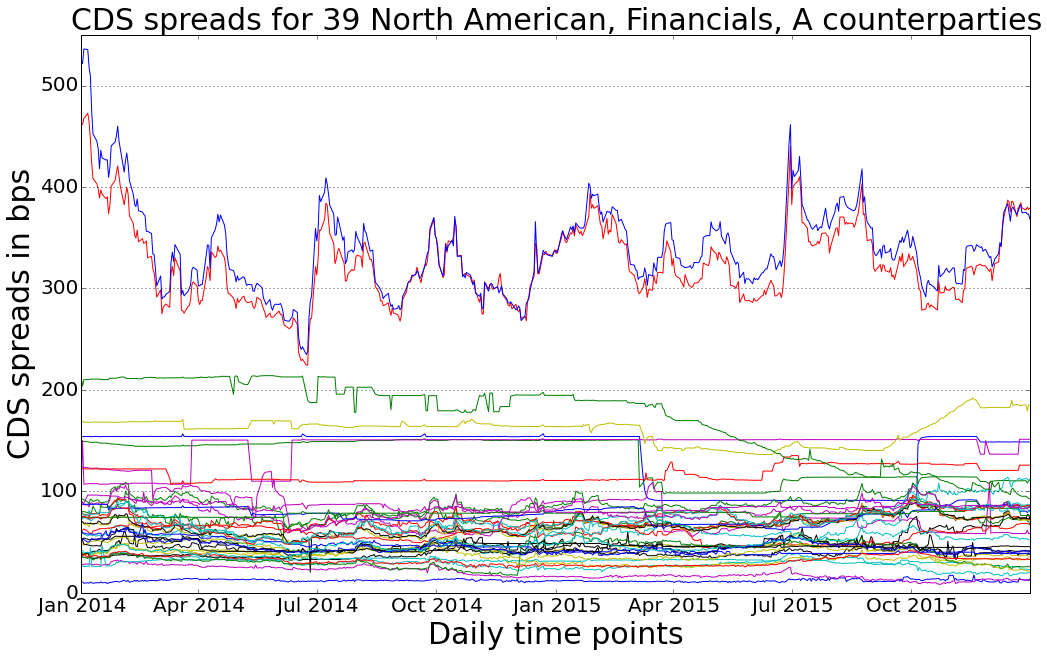

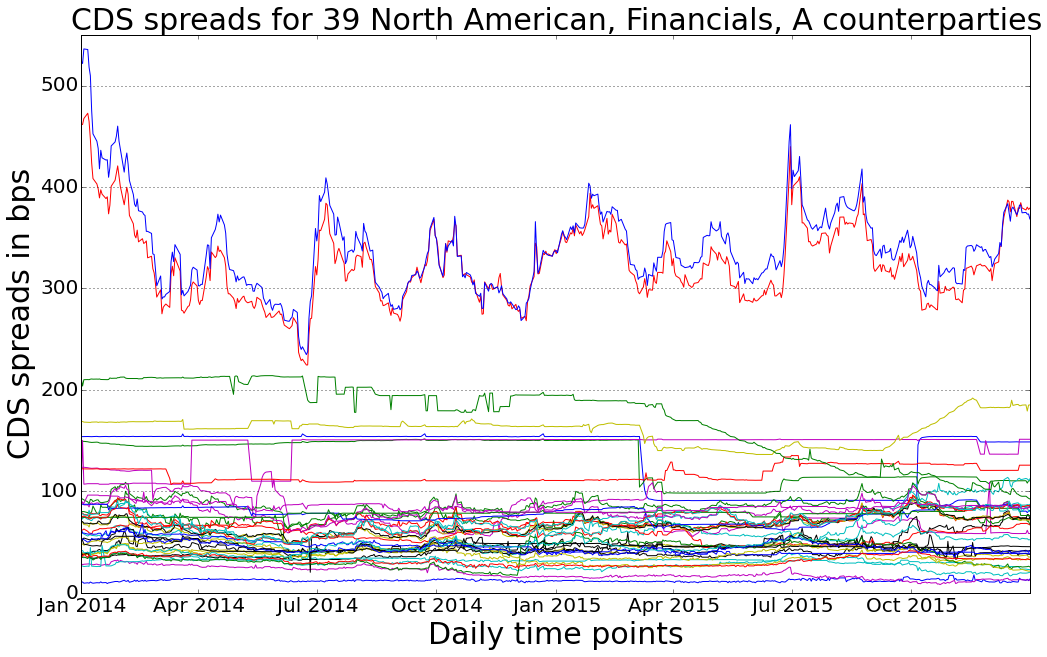

The research article on “Liquidity risk in derivatives valuation: an improved credit proxy method” by Dr. Sumit Sourabh (CSL, UvA), Dr. Markus Hofer (ING Bank) and Prof. Drona Kandhai (ING Bank and CSl, UvA) was recently published in Quantitative Finance.

The main contribution of the paper is a novel proxy methodology for liquidity risk using equity returns, which is significantly more accurate compared to both existing methodologies, and produces more reliable, stable and robust market risk and capital measures, and credit valuation adjustment. For more details see http://www.tandfonline.com/doi/full/10.1080/14697688.2017.1315166