The research article on “Incorporating Contagion in Portfolio Credit Risk Models Using Network Theory” by Ioannis Anagnostou, Sumit Sourabh, and Drona Kandhai was recently published in Complexity.

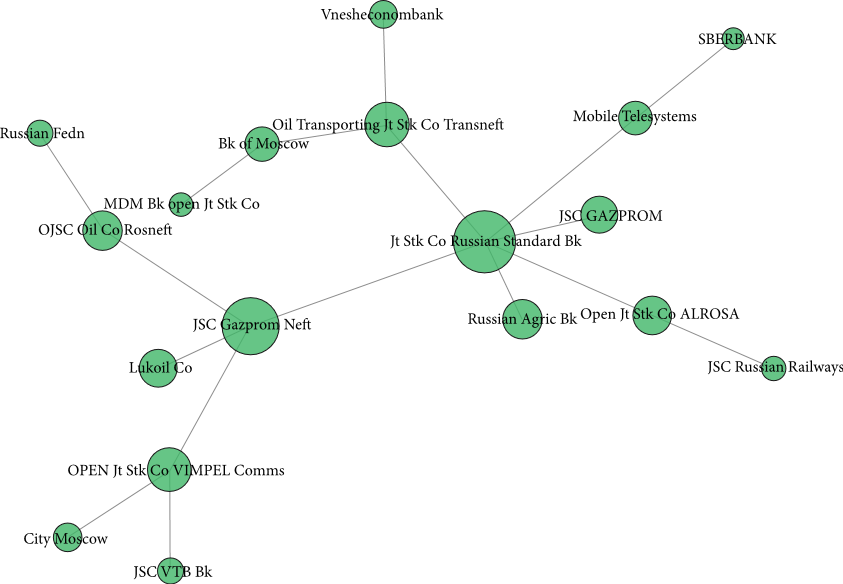

“Portfolio credit risk models estimate the range of potential losses due to defaults or deteriorations in credit quality. Most of these models perceive default correlation as fully captured by the dependence on a set of common underlying risk factors. In light of empirical evidence, the ability of such a conditional independence framework to accommodate for the occasional default clustering has been questioned repeatedly. Thus, financial institutions have relied on stressed correlations or alternative copulas with more extreme tail dependence. In this paper, we propose a different remedy—augmenting systematic risk factors with a contagious default mechanism which affects the entire universe of credits. We construct credit stress propagation networks and calibrate contagion parameters for infectious defaults. The resulting framework is implemented on synthetic test portfolios wherein the contagion effect is shown to have a significant impact on the tails of the loss distributions.”

For more details please see https://www.hindawi.com/journals/complexity/2018/6076173/