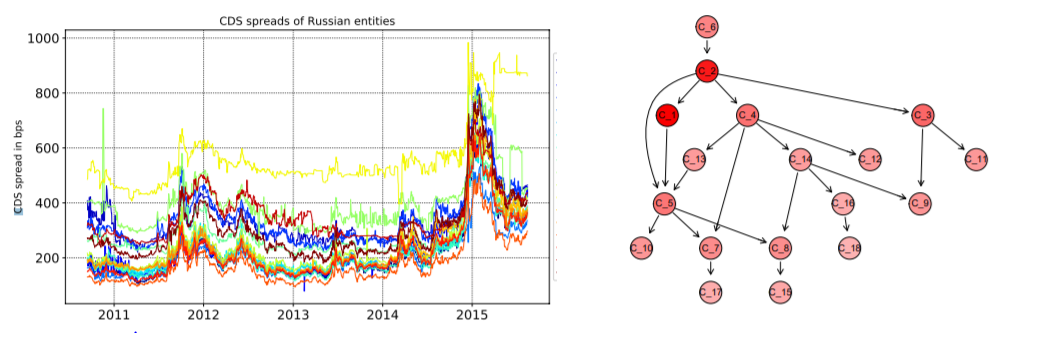

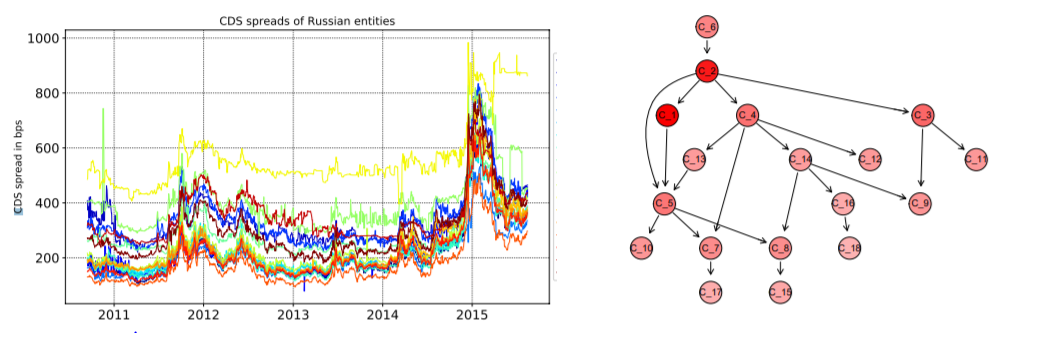

Sumit Sourabh, Markus Hofer and Drona Kandhai develop a novel framework using Bayesian networks to capture distress dependence in the context of counterparty credit risk. Then, they apply this methodology to a wrong-way risk model and stress-scenario testing. Their results show that stress propagation in an interconnected financial system can have a significant impact on counterparty credit exposures.

Their article can be found here.